The semiconductor market is projected to grow from $600 Billion in 2024 at a compound annual growth rate (CAGR) of 8.6%, surpassing $1 trillion by 2030. Growth reflects a structural shift driven by increased semiconductor content per system, greater compute intensity, and widespread AI adoption across end markets. Growth now depends more on technology adoption and silicon value per device than on unit volumes. Meanwhile, inventory normalization and changing supply chain dynamics are influencing near-term results. To distinguish between durable and cyclical growth, it is important to analyze demand trends in key end markets. The table below summarizes these trends and sets the stage for further discussion on inventory, emerging growth areas, and the future of the semiconductor industry.

End Market

CAGR (24–30F)

Key Trends

Semiconductor Content

Growth & Outlook

Automotive

~10.7%

- Electrification (EVs)

- Autonomous driving & ADAS

- Software-defined vehicles

- SiC & GaN power devices

- HPC SoCs for ADAS/autonomy

- Sensors (radar, LiDAR, cameras)

- Connectivity ICs & ECUs

- PMICs

- Chip count per vehicle rising

- ASP per chip increasing

- Growth persists even with flat auto volumes

- ICE & chassis electronics gradually decline

Server & Network

~11.6%

- GenAI and AI automation

- Hyperscale & AI data centers

- Rising data traffic

- CPUs, GPUs, AI accelerators

- DPUs, HBM & DDR5

- Networking ICs

- GaN RF & power ICs

- Strong growth in servers & accelerators

- Custom AI silicon adoption rising

- Telecom grows steadily with limited chip-share upside

Home Appliances & Wearables

5.6%

- AI-enabled smart appliances

- IoT connectivity

- Wearables adoption

- AI processors & MCUs

- PMICs

- Connectivity ICs

- Sensors & wearable SoCs

- Incremental silicon growth

- TVs & major appliances drive upside

- Wearables add sensor & edge-AI content

End Market

CAGR (24–30F)

Key Trends

Semiconductor Content

Growth & Outlook

Automotive

~10.7%

- Electrification (EVs)

- Autonomous driving & ADAS

- Software-defined vehicles

- SiC& GaN power devices

- HPC SoCs for ADAS/autonomy

- Sensors (radar, LiDAR, cameras)

- Connectivity ICs & ECUs

- PMICs

- Chip count per vehicle rising

- ASP per chip increasing

- Growth persists even with flat auto volumes

- ICE & chassis electronics gradually decline

Server & Network

~11.6%

- GenAI and AI automation

- Hyperscale & AI data centers

- Rising data traffic

- CPUs, GPUs, AI accelerators

- DPUs, HBM & DDR5

- Networking ICs

- GaN RF & power ICs

- Strong growth in servers & accelerators

- Custom AI silicon adoption rising

- Telecom grows steadily with limited chip-share upside

Home Appliances & Wearables

5.6%

- AI-enabled smart appliances

- IoT connectivity

- Wearables adoption

- AI processors & MCUs

- PMICs

- Connectivity ICs

- Sensors & wearable SoCs

- Incremental silicon growth

- TVs & major appliances drive upside

- Wearables add sensor & edge-AI content

Computing Devices (PCs & Smartphones)

5.5%

- AI PCs & AI smartphones

- Edge AI adoption

- Premiumization

- Application processors (CPU/GPU/NPU)

- ISPs

- LPDDR memory

- PMICs

- Smartphones behave like compact computers

- High-end models outperform low-end

- Rising semiconductor share of COGS

Industrial – Overall

High single digit (durable)

- Automation & smart factories

- Energy transition

- Healthcare & defense spend

- Industrial MCUs & CPUs

- ASICs & edge-AI chips

- Sensors & connectivity ICs

- SiC power & GaN RF

- Broad, stable demand

- Long qualification cycles

- Strategic, resilient growth through 2026+

Medical Devices

~5.8%

- AI diagnostics & imaging

- Remote monitoring

- Surgical automation

- CPUs & GPUs

- AI accelerators

- Biosensors & MEMS

- Analog & power ICs

- Steady, regulated growth

- Rising chip content per system

- High reliability & long lifecycles

Automation Equipment

~8.9%

- Smart factories

- Robotics & machine vision

- Edge computing

- Industrial MCUs & CPUs

- ASICs

- Sensors & connectivity ICs

- Core industrial growth engine

- Content-driven expansion

- Strong visibility

Smart Agriculture Equipment

~17.3%

- Precision farming

- IoT & sensors everywhere

- AI-driven yield optimization

- Sensors (soil, climate, vision)

- MCUs & edge-AI chips

- Connectivity ICs

- Fastest-growing industrial sub-segment

- Low base, high digital penetration upside

Defense Equipment

~8.2%

- Rising geopolitical risk

- Unmanned systems

- Advanced radar & EW

- GaN RF

- Secure processors • Edge AI chips

- Ruggedized & ceramic packaging

- Semiconductor demand rising faster than unit growth

- Strategic, budget-backed spending

Renewable Energy

~13.4%

- Energy transition

- Grid modernization

- Storage & power conversion

- SiC power devices

- Analog ICs

- Sensors & connectivity ICs

- Strong multi-year growth

- Power semiconductors are key value driver

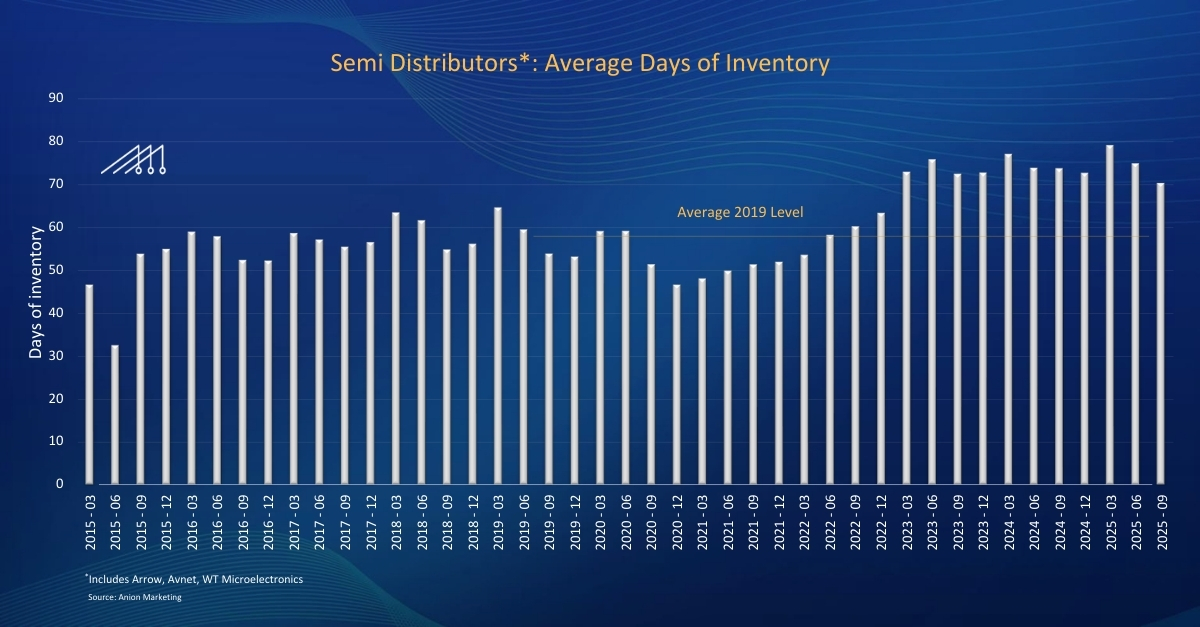

Semiconductor Inventory Trends

Supply-chain inventory is finally moving in the right direction. In Q3’25, total days of inventory (DOI) fell more than normal seasonality, signaling destocking pressure is easing. Inventory is still above historical levels, but the trend supports a gradual normalization through 2026, driven by improving demand and the start of a replenishment cycle.

Key Points

- Shift from depletion to builds: There is a clear shift from inventory depletion to inventory builds. Distributor responses show fewer expectations to draw down stock and a growing willingness to rebuild inventory across product lines.

- Channel + customer behavior improving: Channel and customer inventories are leaner. After multiple quarters of drawdowns, respondents point to improved balance sheets and greater readiness to restock.

- Auto is the swing factor: Auto inventories are below long-term averages, increasing the likelihood of a replenishment cycle as auto demand converges with other end markets.

- Macro/geopolitics still distort ordering: Ordering behavior remains cautious but is improving. Macro and geopolitical uncertainty still influence short-cycle ordering, while producers maintain higher buffers, but the overall direction is constructive.

- Tightness catalysts: Rising constraints, driven by memory shortages and supplier-specific disruptions alongside improving end-market demand, increase the probability that restocking accelerates once lead times extend further.

What’s Next in Semiconductors?

The next wave of semiconductor growth is expanding beyond traditional end markets into new compute-heavy platforms. What connects these themes is rising silicon intensity. Each application pushes higher requirements for real-time compute, sensing, connectivity, power efficiency, and reliability. Some are already scaling in the market today, while others are earlier-stage but strategically important because they pull through high-value silicon content and specialized design.

Near-term momentum is concentrated in platforms where feasibility and market readiness are both high. Advanced AI is the anchor, and it is pulling entire stacks forward, including memory bandwidth, networking, power delivery, and advanced packaging. Driverless autonomy and humanoid robots extend this AI wave into the physical world, requiring continuous sensing and low-latency decision-making. Quantum computing and brain-computer interfaces are earlier, but the semiconductor demand is clear in control electronics, interfaces, security, and specialized analog.

Separately, space exploration, urban air mobility, and hyperloop or maglev are longer-dated opportunities. Their semiconductor content can be very high, but timing depends on economics, regulation, safety qualification, and infrastructure buildout.

Growth Areas

Humanoid Robots

- A new platform that combines edge AI compute with dense sensing and precise motor control.

- Semiconductor stack includes AI SoCs and NPUs, multi-sensor fusion (vision, IMU, ToF/LiDAR), connectivity, and power management.

- Success depends on energy-efficient compute, thermal control, and tight hardware-software integration.

Driverless Autonomy

- Real-time perception and decision-making drive higher compute density and sensor content.

- Semiconductor demand spans ADAS and sensor-fusion SoCs, radar and imaging sensors, automotive connectivity, and safety-grade MCUs.

- Strong silicon content growth even when vehicle volumes are flat because autonomy increases chips per system.

Space Exploration

- High-reliability and harsh-environment electronics increase demand for specialized silicon.

- Key areas include radiation-tolerant compute, secure communications, RF front-end, power management, and rugged packaging.

- Growth tied to satellite constellations, onboard processing, and mission-critical connectivity.

.png)

Urban Air Mobility (eVTOL)

- Electrified propulsion plus aviation safety requirements create a high-content silicon stack.

- Demand spans power semiconductors, motor drives, sensing, flight-control compute, redundancy, and secure communications.

- Timing depends on certification, infrastructure, and unit economics, but silicon content per vehicle is high.

Hyperloop and Magnetic Levitation

- Semiconductor opportunities exist in power electronics, sensing, automation control, communications, and safety systems.

- Scale and timing are the main uncertainties due to infrastructure intensity and deployment risk.

- Most likely near-term demand is in pilots and specialized rail upgrades rather than mass rollout.

Brain-Computer Interface

- Early-stage, but highly semiconductor intensive due to signal fidelity and power constraints.

- Requires ultra-low-power analog front ends, precision ADCs, embedded processing, secure connectivity, and specialized packaging.

- Medical-grade reliability and long qualification cycles can create defensible, high-value silicon opportunities.

Turning Insight Into Growth: Be Known, Be Found, Be Chosen

The semiconductor market is on track to exceed $1T by 2030, powered by two structural engines: AI-driven server and networking demand and rising silicon content in automotive and industrial systems. Beyond these core markets, the next wave of growth is forming in compute-heavy platforms such as humanoid robots, driverless autonomy, space exploration, brain-computer interfaces, and next-generation mobility, each pushing higher requirements for compute, sensors, connectivity, power efficiency, and reliability.

Anion Marketing helps semiconductor and deep-tech companies translate these market shifts into measurable growth. We combine market intelligence with execution to help you:

- Be known: Clarify positioning, sharpen messaging, and build credibility through thought leadership and branding

- Be found: Drive always-on visibility and demand capture through content, SEO, ABM, campaigns, and partner channels

- Be chosen: Convert interest into pipeline and wins with enablement, proof points, competitive narratives, and funnel optimization

If you are planning your next growth chapter, we can help you prioritize the right opportunities and build a repeatable engine for new customer acquisition.

Add comments…

0

Add comments…

About Author

The semiconductor market is projected to grow from $600 Billion in 2024 at a compound annual growth rate (CAGR) of 8.6%, surpassing $1 trillion by 2030. Growth reflects a structural shift driven by increased semiconductor content per system, greater compute intensity, and widespread AI adoption across end markets. Growth now depends more on technology adoption and silicon value per device than on unit volumes. Meanwhile, inventory normalization and changing supply chain dynamics are influencing near-term results. To distinguish between durable and cyclical growth, it is important to analyze demand trends in key end markets. The table below summarizes these trends and sets the stage for further discussion on inventory, emerging growth areas, and the future of the semiconductor industry.

End Market

CAGR (24–30F)

Key Trends

Semiconductor Content

Growth & Outlook

Automotive

~10.7%

• Electrification (EVs)

• Autonomous driving & ADAS

• Software-defined vehicles

• Autonomous driving & ADAS

• Software-defined vehicles

• SiC & GaN power devices

• HPC SoCs for ADAS/autonomy

• Sensors (radar, LiDAR, cameras)

• Connectivity ICs & ECUs

• PMICs

• HPC SoCs for ADAS/autonomy

• Sensors (radar, LiDAR, cameras)

• Connectivity ICs & ECUs

• PMICs

• Chip count per vehicle rising

• ASP per chip increasing

• Growth persists even with flat auto volumes

• ICE & chassis electronics gradually decline

• ASP per chip increasing

• Growth persists even with flat auto volumes

• ICE & chassis electronics gradually decline

Server & Network

~11.6%

• GenAI and AI automation

• Hyperscale & AI data centers

• Rising data traffic

• Hyperscale & AI data centers

• Rising data traffic

• CPUs, GPUs, AI accelerators

• DPUs, HBM & DDR5

• Networking ICs

• GaN RF & power ICs

• DPUs, HBM & DDR5

• Networking ICs

• GaN RF & power ICs

• Strong growth in servers & accelerators

• Custom AI silicon adoption rising

• Telecom grows steadily with limited chip-share upside

• Custom AI silicon adoption rising

• Telecom grows steadily with limited chip-share upside

Home Appliances & Wearables

5.6%

• AI-enabled smart appliances

• IoT connectivity

• Wearables adoption

• IoT connectivity

• Wearables adoption

• AI processors & MCUs

• PMICs

• Connectivity ICs

• Sensors & wearable SoCs

• PMICs

• Connectivity ICs

• Sensors & wearable SoCs

• Incremental silicon growth

• TVs & major appliances drive upside

• Wearables add sensor & edge-AI content

• TVs & major appliances drive upside

• Wearables add sensor & edge-AI content

End Market

CAGR (24–30F)

Key Trends

Semiconductor Content

Growth & Outlook

Automotive

~10.7%

- Electrification (EVs)

- Autonomous driving & ADAS

- Software-defined vehicles

- SiC& GaN power devices

- HPC SoCs for ADAS/autonomy

- Sensors (radar, LiDAR, cameras)

- Connectivity ICs & ECUs

- PMICs

- Chip count per vehicle rising

- ASP per chip increasing

- Growth persists even with flat auto volumes

- ICE & chassis electronics gradually decline

Server & Network

~11.6%

- GenAI and AI automation

- Hyperscale & AI data centers

- Rising data traffic

- CPUs, GPUs, AI accelerators

- DPUs, HBM & DDR5

- Networking ICs

- GaN RF & power ICs

- Strong growth in servers & accelerators

- Custom AI silicon adoption rising

- Telecom grows steadily with limited chip-share upside

Home Appliances & Wearables

5.6%

- AI-enabled smart appliances

- IoT connectivity

- Wearables adoption

- AI processors & MCUs

- PMICs

- Connectivity ICs

- Sensors & wearable SoCs

- Incremental silicon growth

- TVs & major appliances drive upside

- Wearables add sensor & edge-AI content

Computing Devices (PCs & Smartphones)

5.5%

- AI PCs & AI smartphones

- Edge AI adoption

- Premiumization

- Application processors (CPU/GPU/NPU)

- ISPs

- LPDDR memory

- PMICs

- Smartphones behave like compact computers

- High-end models outperform low-end

- Rising semiconductor share of COGS

Industrial – Overall

High single digit (durable)

- Automation & smart factories

- Energy transition

- Healthcare & defense spend

- Industrial MCUs & CPUs

- ASICs & edge-AI chips

- Sensors & connectivity ICs

- SiC power & GaN RF

- Broad, stable demand

- Long qualification cycles

- Strategic, resilient growth through 2026+

Medical Devices

~5.8%

- AI diagnostics & imaging

- Remote monitoring

- Surgical automation

- CPUs & GPUs

- AI accelerators

- Biosensors & MEMS

- Analog & power ICs

- Steady, regulated growth

- Rising chip content per system

- High reliability & long lifecycles

Automation Equipment

~8.9%

- Smart factories

- Robotics & machine vision

- Edge computing

- Industrial MCUs & CPUs

- ASICs

- Sensors & connectivity ICs

- Core industrial growth engine

- Content-driven expansion

- Strong visibility

Smart Agriculture Equipment

~17.3%

- Precision farming

- IoT & sensors everywhere

- AI-driven yield optimization

- Sensors (soil, climate, vision)

- MCUs & edge-AI chips

- Connectivity ICs

- Fastest-growing industrial sub-segment

- Low base, high digital penetration upside

Defense Equipment

~8.2%

- Rising geopolitical risk

- Unmanned systems

- Advanced radar & EW

- GaN RF

- Secure processors • Edge AI chips

- Ruggedized & ceramic packaging

- Semiconductor demand rising faster than unit growth

- Strategic, budget-backed spending

Renewable Energy

~13.4%

- Energy transition

- Grid modernization

- Storage & power conversion

- SiC power devices

- Analog ICs

- Sensors & connectivity ICs

- Strong multi-year growth

- Power semiconductors are key value driver

Semiconductor Inventory Trends

Supply-chain inventory is finally moving in the right direction. In Q3’25, total days of inventory (DOI) fell more than normal seasonality, signaling destocking pressure is easing. Inventory is still above historical levels, but the trend supports a gradual normalization through 2026, driven by improving demand and the start of a replenishment cycle.

Key points

- Shift from depletion to builds: There is a clear shift from inventory depletion to inventory builds. Distributor responses show fewer expectations to draw down stock and a growing willingness to rebuild inventory across product lines.

- Channel + customer behavior improving: Channel and customer inventories are leaner. After multiple quarters of drawdowns, respondents point to improved balance sheets and greater readiness to restock.

- Auto is the swing factor: Auto inventories are below long-term averages, increasing the likelihood of a replenishment cycle as auto demand converges with other end markets.

- Macro/geopolitics still distort ordering: Ordering behavior remains cautious but is improving. Macro and geopolitical uncertainty still influence short-cycle ordering, while producers maintain higher buffers, but the overall direction is constructive.

- Tightness catalysts: Rising constraints, driven by memory shortages and supplier-specific disruptions alongside improving end-market demand, increase the probability that restocking accelerates once lead times extend further.

What’s Next in Semiconductors?

The next wave of semiconductor growth is expanding beyond traditional end markets into new compute-heavy platforms. What connects these themes is rising silicon intensity. Each application pushes higher requirements for real-time compute, sensing, connectivity, power efficiency, and reliability. Some are already scaling in the market today, while others are earlier-stage but strategically important because they pull through high-value silicon content and specialized design.

Near-term momentum is concentrated in platforms where feasibility and market readiness are both high. Advanced AI is the anchor, and it is pulling entire stacks forward, including memory bandwidth, networking, power delivery, and advanced packaging. Driverless autonomy and humanoid robots extend this AI wave into the physical world, requiring continuous sensing and low-latency decision-making. Quantum computing and brain-computer interfaces are earlier, but the semiconductor demand is clear in control electronics, interfaces, security, and specialized analog.

Separately, space exploration, urban air mobility, and hyperloop or maglev are longer-dated opportunities. Their semiconductor content can be very high, but timing depends on economics, regulation, safety qualification, and infrastructure buildout.

Growth Areas

Humanoid Robots

- A new platform that combines edge AI compute with dense sensing and precise motor control.

- Semiconductor stack includes AI SoCs and NPUs, multi-sensor fusion (vision, IMU, ToF/LiDAR), connectivity, and power management.

- Success depends on energy-efficient compute, thermal control, and tight hardware-software integration.

- A new platform that combines edge AI compute with dense sensing and precise motor control.

- Semiconductor stack includes AI SoCs and NPUs, multi-sensor fusion (vision, IMU, ToF/LiDAR), connectivity, and power management.

- Success depends on energy-efficient compute, thermal control, and tight hardware-software integration.

Driverless Autonomy

- Real-time perception and decision-making drive higher compute density and sensor content.

- Semiconductor demand spans ADAS and sensor-fusion SoCs, radar and imaging sensors, automotive connectivity, and safety-grade MCUs.

- Strong silicon content growth even when vehicle volumes are flat because autonomy increases chips per system.

Space Exploration

- High-reliability and harsh-environment electronics increase demand for specialized silicon.

- Key areas include radiation-tolerant compute, secure communications, RF front-end, power management, and rugged packaging.

- Growth tied to satellite constellations, onboard processing, and mission-critical connectivity.

- High-reliability and harsh-environment electronics increase demand for specialized silicon.

- Key areas include radiation-tolerant compute, secure communications, RF front-end, power management, and rugged packaging.

- Growth tied to satellite constellations, onboard processing, and mission-critical connectivity.

Urban Air Mobility (eVTOL)

- Electrified propulsion plus aviation safety requirements create a high-content silicon stack.

- Demand spans power semiconductors, motor drives, sensing, flight-control compute, redundancy, and secure communications.

- Timing depends on certification, infrastructure, and unit economics, but silicon content per vehicle is high.

Hyperloop and Magnetic Leviation

- Semiconductor opportunities exist in power electronics, sensing, automation control, communications, and safety systems.

- Scale and timing are the main uncertainties due to infrastructure intensity and deployment risk.

- Most likely near-term demand is in pilots and specialized rail upgrades rather than mass rollout.

- Semiconductor opportunities exist in power electronics, sensing, automation control, communications, and safety systems.

- Scale and timing are the main uncertainties due to infrastructure intensity and deployment risk.

- Most likely near-term demand is in pilots and specialized rail upgrades rather than mass rollout.

Brain-Computer Interface

- Early-stage, but highly semiconductor intensive due to signal fidelity and power constraints.

- Requires ultra-low-power analog front ends, precision ADCs, embedded processing, secure connectivity, and specialized packaging.

- Medical-grade reliability and long qualification cycles can create defensible, high-value silicon opportunities.

Turning Insight into Growth: Be Known, Be Found, Be Chosen

The semiconductor market is on track to exceed $1T by 2030, powered by two structural engines: AI-driven server and networking demand and rising silicon content in automotive and industrial systems. Beyond these core markets, the next wave of growth is forming in compute-heavy platforms such as humanoid robots, driverless autonomy, space exploration, brain-computer interfaces, and next-generation mobility, each pushing higher requirements for compute, sensors, connectivity, power efficiency, and reliability.

Anion Marketing helps semiconductor and deep-tech companies translate these market shifts into measurable growth. We combine market intelligence with execution to help you:

- Be known: Clarify positioning, sharpen messaging, and build credibility through thought leadership and branding

- Be found: Drive always-on visibility and demand capture through content, SEO, ABM, campaigns, and partner channels

- Be chosen: Convert interest into pipeline and wins with enablement, proof points, competitive narratives, and funnel optimization

If you are planning your next growth chapter, we can help you prioritize the right opportunities and build a repeatable engine for new customer acquisition.

.svg)

.png)